Decentralized finance (DeFi) promises a future with greater financial inclusivity, total transparency, and accessibility for users. Aave, a DeFi protocol built on the Ethereum blockchain, has emerged as one of the leading platforms in the space.

Jumping into DeFi can be daunting, as most DeFi protocols require varying degrees of expertise in blockchain tech. However, DeFi apps have become much more user-friendly, and Aave is no exception, including non-traders like myself.

DailyCoin is reviewing major DeFi platforms in the space to promote education on decentralized technology. This comprehensive review covers Aave, its functionalities, strengths, and my perspective on the platform.

What Is Aave?

Aave is an open-source, multi-chain decentralized DeFi lending protocol allowing people to borrow crypto. It operates on the Ethereum blockchain, offering services such as compound interest accrual, yield farming, lending, and borrowing of digital assets.

Source: Aave.com

Source: Aave.com

Essentially, the Aave platform is a system of smart contracts that enables these transactions to occur directly between lenders and borrowers without needing an intermediary.

One of the unique aspects of Aave is its use of aTokens and its native token, AAVE. When users deposit a cryptocurrency into Aave, they receive a corresponding amount of aTokens, representing the deposited assets and accumulating interest in real-time.

The AAVE token, on the other hand, is used for governance of the protocol. AAVE token holders can participate in decision-making, voting on proposals and protocol upgrades.

Which Tokens Does Avee Support?

Aave supports a variety of crypto assets for lending and borrowing. At the time of this review, users can trade major ERC-20 tokens such as ETH, wrapped Bitcoin (wBTC), Shiba Inu, Avalanche, and many others. The Aave protocol also supports ERC-20 stablecoins, like DAI, USD Coin (USDC), and Tether USDT.

Does Aave Have KYC?

It is important to note that, like other DeFi platforms, such as Uniswap, Aave does not have a Know Your Customer (KYC) process. Unlike centralized exchanges like Coinbase and Binance, users don’t have to show their IDs when trading. This means anyone can interact with the protocol if they have an Ethereum wallet.

Source: Aave.com

Source: Aave.com

This lack of KYC is a double-edged sword; on one hand, it allows for greater privacy and inclusivity, but on the other, it could potentially attract malicious actors. As a result, users need to be extra cautious when transacting on the Aave platform, ensuring they understand the associated risks and have secure wallet practices.

History of Aave

The journey of Aave is an interesting one that is deeply intertwined with the evolution of DeFi itself. The platform began as ETHLend, a simple peer-to-peer lending platform on the Ethereum blockchain, founded by Stani Kulechov in 2017.

Source: Web Summit, Flickr

Source: Web Summit, Flickr

ETHLend was an early mover in the DeFi space and was one of the first platforms to offer secure, trustless crypto loans using Ethereum smart contracts.

In 2018, ETHLend conducted an initial coin offering (ICO) and raised funds to develop its platform further. Then, in 2020, ETHLend rebranded to Aave and launched Aave V1, introducing several innovative features such as flash loans, rate-switching, and aTokens. The rebranding represented a shift from a peer-to-peer lending platform to a liquidity pool-based model, which has since become a standard in DeFi.

Aave’s growth has been rapid since then, with the platform introducing Aave V2 in 2021, which brought even more features and improvements, such as credit delegation, collateral swapping, and native credit default swaps. The platform’s governance token, AAVE, was also introduced, decentralizing control of the protocol to its users.

User Experience on Aave

As someone not deeply immersed in trading, I found the user interface of Aave refreshingly intuitive. It offers an uncluttered design and clear navigation, a relief for a beginner like me.

The process – from depositing funds into a lending pool and borrowing against collateral to tracking the earned interest – is all straightforward.

A minor caveat is that some understanding of blockchain technology is necessary to fully utilize the platform. It wasn’t a steep learning curve, but a learning curve nonetheless.

Key Features of Aave

Aave’s features set it apart from other DeFi protocols, making it appealing even to non-traders.

Lending and Borrowing: As someone looking for passive income avenues, the Aave lending option was a pleasant discovery. The platform allows users to lend assets and earn interest, while others can borrow these same assets.

Interest Rates: Aave’s dual offering of stable and variable interest rates gives users the flexibility to choose based on crypto market conditions. This feature was handy during volatile market conditions, offering a stable interest option.

Flash Loans: The concept of flash loans was new to me, but it’s an innovative feature that allows uncollateralized loans, as long as they are returned within the same transaction block. While I haven’t personally used this feature, it’s an interesting offering for those looking to execute complex strategies.

aTokens: Upon depositing assets, users receive aTokens. These aTokens represent the deposited assets and earn interest in real-time, providing a simple way to keep track of one’s earnings.

Governance: AAVE token holders are a part of the decision-making process, voting on new proposals and protocol upgrades. The system is similar to owning shares in a publicly traded company.

Source: Aave.com

Source: Aave.com

Aave Fees

Aave’s fee structure is relatively straightforward. When you borrow cryptocurrencies on the platform, you’ll be charged a fee of 0.01%. The rate is a bit higher for flash loans, which are uncollateralized loans that must be returned within the same transaction, at 0.09%. However, it’s important to note that these are the fees charged by Aave itself.

Source: Aave.com

Source: Aave.com

When conducting transactions on the Ethereum network, which Aave is built upon, you’ll also need to pay Ethereum transaction fees or gas fees. These fees fluctuate based on network congestion and can sometimes be quite high, especially during periods of heavy usage.

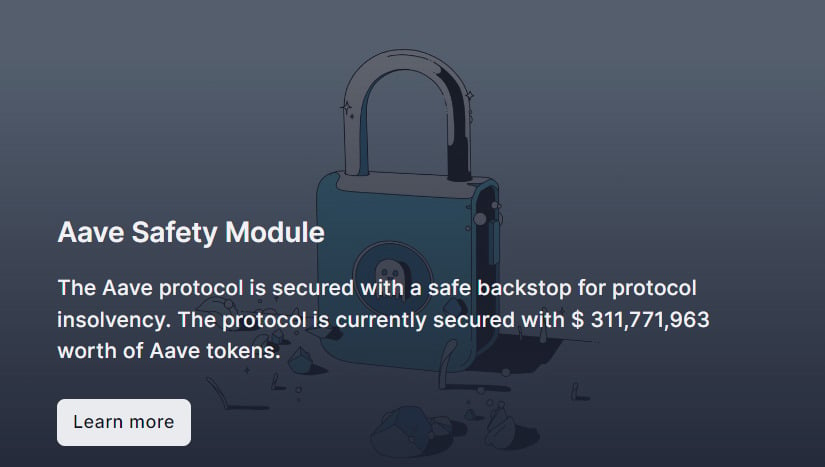

Security

For a non-trader like myself, the security of my assets is paramount. Leading security firms have audited Aave’s smart contracts, and the platform has a safety module that provides a backstop for protocol insolvency.

The bug bounty program further enhances security by incentivizing the community to find and fix potential vulnerabilities.

Source: Aave.com

Source: Aave.com

Still, security measures were not enough to deter hackers. In April 2023, Aave suffered a major flash loan exploit, resulting in $10 million in user funds lost.

Community and Support

Aave’s community is vast and diverse, with over 161,000 token holders. The Aave Grants DAO is a testament to the strength of the community. It’s a program that funds ideas from the community for the further development of the protocol. However, I found that getting direct customer support can be challenging, with most assistance coming from community forums and discussions.

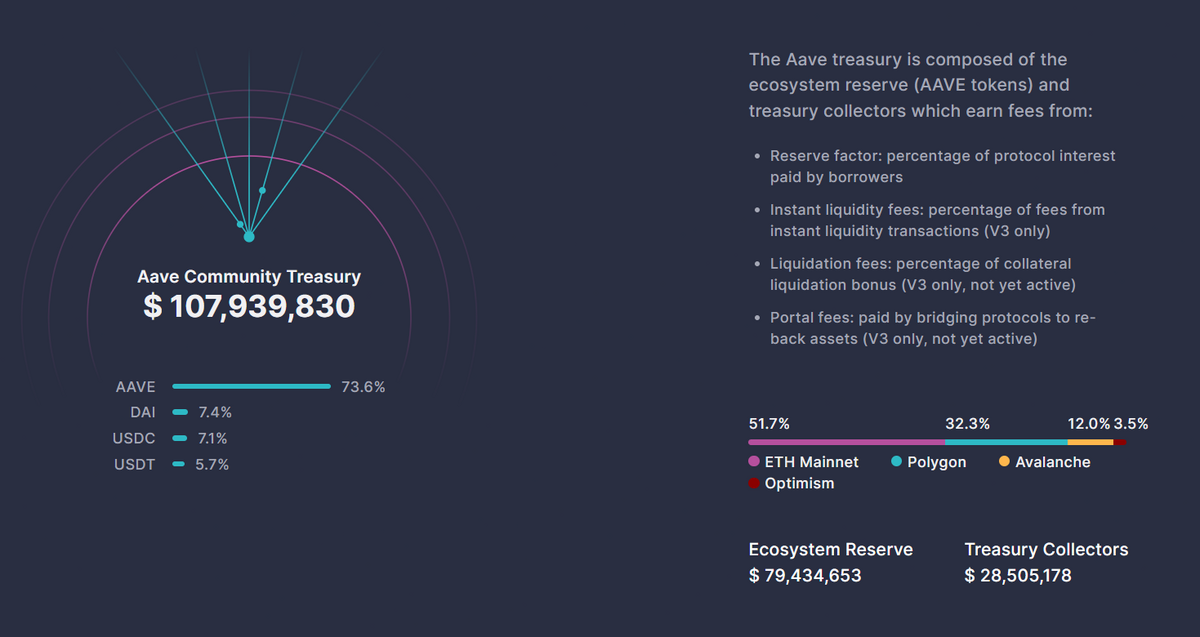

Treasury and Earnings

The Aave treasury is an interesting, more complex feature than it initially appears. It comprises the ecosystem reserve (AAVE tokens) and treasury collectors, which earn fees from various sources. As a non-trader, understanding how these earnings and fees interact and impact the overall value of the platform was a learning experience.

Pros and Cons of Aave

From a non-trader’s perspective, Aave has proven to be a robust and reliable DeFi platform. It strongly emphasizes community governance and security, which I value greatly.

However, it requires some understanding of blockchain technology and DeFi concepts, which can be challenging for beginners.

Pros

- User-friendly interface, even for non-traders.

- Innovative features like Flash Loans and aTokens provide opportunities beyond traditional trading.

- Strong community governance allows for participation in decision-making.

- Emphasis on security provides a level of comfort for asset protection.

Cons

- Requires a certain level of blockchain knowledge to utilize the platform fully.

- Customer support is largely community-based, which can be hit-or-miss.

- Potential smart contract risks, inherent in DeFi, should be considered.

In the end, my journey with Aave has been a positive one. It has shown me that the world of DeFi is not just for seasoned traders. Individuals like myself, simply looking for innovative ways to grow and protect their assets, can also use and benefit from it.

Is Aave for You?

Determining whether Aave is the right platform for you depends on your familiarity with blockchain technology, investment goals, and risk tolerance.

If you’re comfortable with blockchain and DeFi concepts, Aave offers a range of opportunities. It’s suitable for those looking for passive income through interest earnings and those interested in more active strategies like flash loans.

For those looking to participate in the governance of a decentralized protocol, holding AAVE tokens gives you voting rights on the platform’s future direction. This could be an exciting opportunity to be part of shaping a leading DeFi protocol.

On the Flipside

- However, as with any DeFi platform, there are risks involved. Smart contract risks, potential protocol insolvency, and the volatility of the cryptocurrency market are all factors that users need to consider. Customer support largely depends on the community, which might not suit everyone.

- Furthermore, while Aave is user-friendly, it does require a basic understanding of blockchain technology. There’s also a learning curve in understanding its various features and how to utilize them best.

Why this Matters

If you’re comfortable with the technology and looking for innovative ways to earn on your assets or participate in a decentralized financial ecosystem, Aave could be an excellent fit for you.

Related articles

Polygon MATIC Optimism Returns as It Teases Bank Partnership

DeFi Protocol Gamma Strategies Suffers $3.4 Million Attack